Oil Bond Controversy

NDA Government's Claim is Untrue to Blame UPA Era Oil Bonds For Fuel Price Hike

Petrol and diesel prices have gone all time high and hit over Rs 100 per litre. The government is facing clamour from the people to bring the rising price of petrol and diesel down by cutting on high taxes and duties on fuel.

As of now, the petrol and diesel are out of the GST ambit and are wholly under the state and government for the tax levy purpose. If petroleum products are brought under the GST, 28% tax would be collected on them as that is the highest slab in the tax regime. Presently taxes account for 58 per cent of the retail selling price of petrol and 52 per cent of the retail selling price of diesel. 42% of the tax collected goes to the state. The states also add value added tax (VAT). Rajasthan levies the highest VAT on petrol in the country, followed by Madhya Pradesh. That is why the petrol and diesel prices vary from state to state.

Dharmendra Pradhan, the Petroleum Minister before cabinet reshuffle and recently the BJP IT cell national head Amit Malviya said that the government is helpless at tax cutting on fuel to give price benefit to consumers for the reason the outgoing UPA government's legacy of mismanagement. Amit Malviya blatantly blamed the UPA government of Dr Manmohan Singh to have issued oil bonds to the extent of Rs 1.3 lakh crore to oil marketing companies (OMCs) that carried forward as burden of outstanding for the BJP government now in power. Let it be noted that Amit Malviya blamed petrol price hike due to oil bonds issued by the UPA government, but the present NDA government hasn't paid any outstanding oil bonds since March 2015.

Therefore Malviya's claim is all the more untrue. Out of Rs 1.44 lakh crore bonds issued by the UPA government between 2005 and 2010, only two bonds totalling to Rs 3,500 crore matured during the NDA's regime in 2015. The next bond is scheduled to mature in October 2021 as per the NDA's budget document.

Let it be known that first oil bonds were issued during Atal Bihari Vajpayee-led BJP government in 2002. The then Union Petroleum Minister, Ram Naik announced bonds worth Rs 9,000 crore were issued by the Reserve Bank of India (RBI) to liquidate 80% of the oil pool deficit. It is true that the present NDA government inherited the debt but this has been happening since 2002. The NDA government must take note of it.

Earlier the payoffs of subsidies to OMCs used to be in cash by the government. OMCs receiving cash subsidies were not free to fix their own prices for petrol (before 2010) and diesel (before 2015). The OMCs were often selling fuel far below the international market price, often at significant expenditure to themselves. Moreover there was a great fiscal pressure on the government due to the 2008 economic crisis and ongoing Middle East conflict resulted in shooting crude oil prices to $140 a barrel. Continuing with cash subsidies to OMCs was not possible without breaching the benchmark set for fiscal deficit by the government. To keep subsidising oil prices, the government issued oil bonds.

Oil bonds, in particular, are special types of bonds that are issued to OMCs like Indian Oil, Hindustan Petroleum and Bharat Petroleum. These were transferable instruments, allowing these companies to raise immediate cash at the time. The government, being the issuer, would bear the interest payments and redemption at maturity.

These companies received oil bonds from the government in place of cash subsidies.

The governments provide subsidies on certain items as part of their social and political obligations to their people to keep them insulated from the high cost of an item. Petroleum is one such item. Hence the government shares part of the price in the shape of subsidy to make the fuel affordable to the consumer and thus consumers are relieved of cost burden.

But this adds financial burden to the government as it has to pay the OMCs for their under-recoveries. Under-recoveries are the difference between the cost of purchasing crude oil in the international market and selling at lower price in the domestic market. This difference amount due to government subsidy policy has to be paid to OMCs.

Therefore to keep the fuel price affordable the OMCs were compensated by the UPA government by way of issuing oil bonds in lieu of cash subsidy.

Let us first understand what oil bonds are. To begin with, oil bonds are debt instruments. Instead of paying the difference or the subsidised amount in cash to the OMCs the government issued oil bonds as securities to be paid after 10 or 15 years and for this period interest will be paid twice a year in cash to the investor (here the OMCs). Thereby the subsidized money becomes loan money to a government entity which borrows funds for a defined period of time at a fixed interest rate. The investors or lenders (here OMC) are paid a fixed rate of interest on the money borrowed for a fixed period to pay the difference amount of subsidy. The investors have double benefit on lending - the interest on lending and assured ‘pay up’ of principal or base or borrowed amount at the time of maturity of the bond issued as security by the government borrower. Therefore oil bonds are not only debt instruments but also government securities.

In a similar way, bonds or securities are issued by the government to public companies like Food Corporation of India and Fertilizer Companies as a substitute to cash subsidies.

Oil bonds were issued to control the expenditure and, in the process, control the fiscal deficit as debts are not accounted for in the fiscal deficit number. All governments do this in different forms to delay the fiscal burden.

Therefore bonds are issued so as not to breach the fiscal deficit target. Every year, governments run a deficit and it is financed through bonds. And, usually bonds have a long life which could be for 15, 20 or even 30 years. Bonds are government securities and an obligation to pay in future. Due to their long life, they are also handed over to successive governments that are obliged to make these payments whenever due.

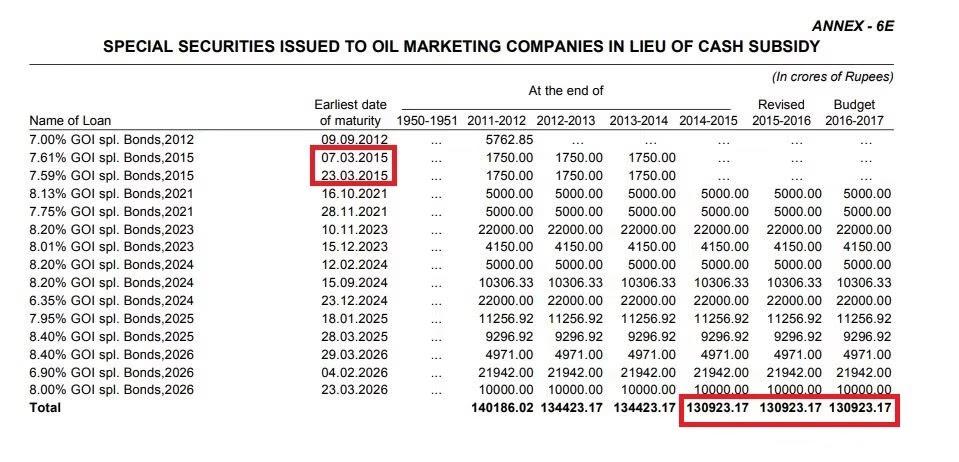

The total worth of these oil bonds was Rs 1.4 lakh crore. The UPA government had paid some amount of bonds. When the NDA government came to power it only inherited Rs 1,30,923.17 crore, to be exact, of debt in terms of the oil bonds that will come up for redemption starting FY2021 till 2026.

Notably, various central and state taxes make up for up to 60% of fuel prices. The central government mopped up Rs 3.72 lakh crore in excise duty on crude oil and petroleum products in the last financial year 2020-21; while the state governments collected Rs 2.03 lakh crore in sales tax and VAT on petrol and diesel. On the other hand, the government has to pay towards the redemption of outstanding oil bonds worth over a lakh crore rupees.

The government has a liability to pay Rs 20,000 crore in the current fiscal year 2021-22 in the form of bond repayment and interest on the outstanding oil bonds. While for the next six years, the government has a total debt obligation worth Rs 1.30 lakh crore.

Modi’s NDA government first came into power in 2014. During its regime, two tranches of bonds, worth Rs 1,750, each (Rs 3,500 crore), matured in 2015.

Two oil bonds will be maturing this fiscal; the government needs to pay Rs 20,000 crore. In 2019, Narendra Modi’s NDA government came into power for the second consecutive time. According to the budget documents, oil bonds worth Rs 41,150 crore are due for maturity between 2019-2024.

In 2018, Union Petroleum Minister Dharmendra Pradhan said that the government has paid around Rs 10,000 crore annually as interest over the last decade. It is likely that the government will pay a similar amount of interest for outstanding bonds for the current fiscal as well. So, the total bond repayment and interest on the outstanding oil bonds stands around Rs 20,000 crore for the current fiscal.

This is not the first time for the NDA government to make such a claim. On September 10, 2018, BJP's official twitter handle claimed that the NDA government repaid pending oil bonds worth Rs 1.3 crore with an interest of Rs 40,000 crore.

However, this was false too because the BJP government paid only Rs 3,500 crore worth of oil bonds which matured in 2015. This means that oil bonds worth Rs 1.3 lakh crore are still pending.

The UPA and the NDA government have been paying interest on oil bonds for the last 20 years. In its second term, the UPA government paid a total of Rs 53,163 crore in interest for oil bonds in the five-year period between 2009-10 and 2013-14. Whereas, the current NDA government paid a total of Rs 40,225 crore between 2014-15 and 2017-18. The interest payment for 2018-19 was budgeted at Rs 9,989.96 crore. This outstanding amount has not changed since 2015-16.

As for the current financial year, Rs 5,000 crore of bonds are due to be repaid on October 16 and November 28, 2021, respectively. This totals to Rs 10,000 crore. This means that Rs 10,000 crore worth of bonds of the total Rs 1,30,923 crore of oil bonds, will be repaid during this financial year. In the current financial year, the government roughly needs around Rs 10,000 crore + interest amount of Rs 9,989.96 = Rs 19,989.96 crore in total.

Petrol prices were determined by the UPA government and were revised every fortnight. In 2014 the price of diesel was also deregulated and since 2017 prices are being revised on a daily basis. Taxation on fuel prices has sharply increased since then and that is why the nation had a series of price hikes during recent past months.

Thereby, the Modi government has increased Central Taxes on petrol & diesel by ₹23.87 & ₹28.37/litre. Excise on Petrol & Diesel was ₹9.20 & ₹3.46 per litre in UPA. BJP Govt increased that by 258% & 820%, respectively.

In 2014-15, when the NDA government came to power, the central excise duty collected was Rs 29,279 crore on petrol and Rs 42,881 crore, according to a response by outgoing Minister of State for Finance after recent reshuffle, Anurag Thakur in the Lok Sabha on March 22, 2021.

Between April 2020 and January 2021, Rs 89,575 crore had been collected as excise duty on petrol and Rs 2,04,906 crore on diesel. This is more than a 400% increase.

The government informed Parliament as late as on 19th July. 2021 that the total excise duty on petrol, diesel and natural gas rose from Rs 53,000 crore in 2013-14 to Rs 2,95,201 crore in April 2021. Rs 94,000 crore the government earned on excise between April and June, ie, during the severe second wave of COVID-19.

Therefore it is possible for the government to give price benefits to consumers. It is possible for the government to hold inflation by giving relief to consumers on fuel prices.

India's fiscal deficit was at 9.3% of GDP for 2020-21, which was the highest fiscal deficit on record. But, as outgoing Petroleum Minister, Dharmendra Pardhan said, levies on fuel is helping Centre afford the current welfare expenditure. It is a known fact that the hike in fuel price is one of the major causes of inflation. The government needs to explain if she is willing to spend more due to inflated costs resulting from sky high prices of fuel. Can the country afford to waste the earnings by taxing more and wasting more?

Let's see how the government is earning on heavily taxed fuel.

In fact, the base price of petrol has only reduced — from Rs 47.12 in May 2014 to Rs 37.29 in June 2021 and central taxes increased from Rs 10.39 in May 2014 to Rs 32.9 in June 2021, according to data from Petroleum Planning and Analysis Cell.

As per the data from the Controller General of Accounts (CGA), excise duty collection during April-November 2020 was at Rs 1,96,342 crore, up from the Rs 1,32,899 crore during the same period in 2019.

This is when both diesel and petrol consumption dropped due to lockdown in the Corona pandemic during these eight months. According to the Petroleum Planning and Analysis Cell (PPAC), diesel sales stood at 44.8 million tonnes in April-Nov 2020, compared to 55.4 million tonnes a year back. Similarly, petrol usage also dropped to 20.4 million tonnes in the eight months this year from 17.4 million tonnes in April-Nov 2019.

"By not reducing taxes the government is able to earn higher revenue and we have seen last year that the excise collections were much higher than what was targeted," said Madan Sabnavis, chief economist at CARE Ratings Ltd, a credit analysis and research company.

The impact of high fuel taxes on the economy was also highlighted by Reserve Bank of India Governor Shaktikahnta Das in a recent meeting. Das said, "Proactive supply side measures, particularly in enabling a calibrated unwinding of high indirect taxes on petrol and diesel – in a coordinated manner by centre and states – are critical to contain further build-up of cost-pressures in the economy."

The rise in fuel prices is increasing transportation costs across the country and even if crude prices drop this may not come down. Considering that almost every single commodity is transported by road at some stage, transportation costs are embedded into all costs.

The central government has been pushing alternative ways to reduce the cost of fuel prices. Under the National Policy on Biofuels 2018 the government emphasised on achieving energy security of the country with a target of reducing import dependence. The government recently fast-tracked its target for selling petrol with 20% blended ethanol to April 1, 2023.

Under The National Biofuel Policy 2018, the target for blending ethanol stood at 20% for petrol and five% for diesel by 2030. But implementation of alternative fuels will take time. The government is already promoting alternative fuels and electric vehicles. That will take years to implement. There is no logic in increasing fuel prices that are currently in use. The government will need to do more to encourage alternative fuel, conservation of fossil fuels, or electric vehicles. The subsidies for electric vehicles could increase. But this is not the right time to do that, because the central tax revenues are falling on account of the contraction of the economy.

Right now, is the time to reduce taxes on petrol and diesel, which will also lower the rate of inflation as fuel is an input cost into almost all commodities, which must be transported to reach the consumer.

It is a good analytical view 👍

ReplyDelete